KEY TAKEWAYS

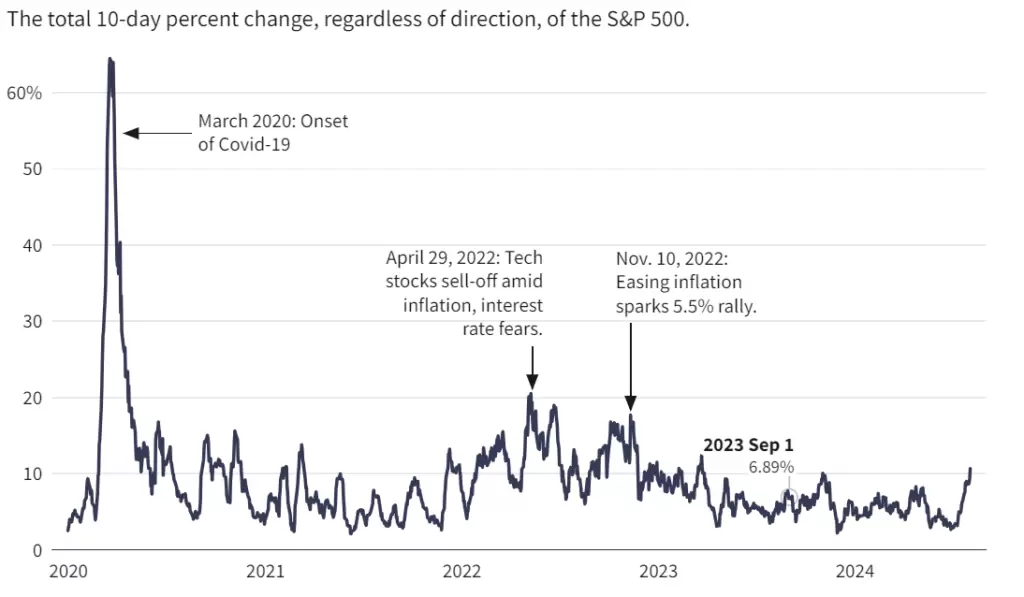

- Stock market volatility has surged in recent weeks. Over the last 10 days, the S&P 500’s average daily move was 1.02%, the highest since March 2023.

- There wasn’t a single day that the S&P 500 moved more than 1% between June 6 and July 9, two days before a soft inflation report surprised Wall Street and boosted expectations for interest rate cuts.

- Earnings, specifically big tech earnings, have exacerbated volatility. This week, when four of the world’s largest tech companies reported quarterly results, there were three days in which the S&P 500 moved more than 1%.

- Investors are also becoming increasingly concerned about the state of the economy, as a series of indicators—notably Friday’s jobs report—have shown activity slowing significantly under the weight of high interest rates.

Stocks tumbled Friday, concluding the most volatile stretch the market has seen in more than a year by some measures.

The S&P 500 shed 1.8% to close lower for the third consecutive week, its longest losing streak since April.

The VIX surged to its highest point all year on Friday after data showed the unemployment rate jumped to 4.3% in July.

It has been nearly a year since stocks experienced swings as violent as the ones seen recently. In the past 10 trading days, there were six sessions in which the S&P 500 rose or fell more than 1%, the most since November.

By another measure, stocks are moving more dramatically now than they have in more than a year. Over the last 10 days, the average daily move was 1.02%, the highest since March 2023.

Why Has Market Volatility Increased?

Last month’s soft inflation report stands out as the primary culprit of all this volatility. There wasn’t a single day that the S&P 500 moved more than 1% between June 6 and July 9, two days before the inflation data surprised Wall Street.

Earnings, specifically big tech earnings, have exacerbated volatility. This week, when four of the world’s largest tech companies reported quarterly results, there were three days in which the S&P 500 rose or fell by more than 1%.

Jitters have set in about high-flying mega-cap tech stocks as investors have become more demanding of market darlings like the Magnificent Seven. For more than a year, most of the group consistently reported double-digit earnings growth as cost cuts, mostly achieved through layoffs and restructuring, boosted their bottom lines.

Now, investors are again concerned about spending, but their focus has shifted. Wall Street was worried about personnel costs in 2022 after tech companies went on a hiring spree to meet peak-pandemic demand.

Today, the problem is infrastructure. Investors balked at surging capital expenditures at tech giants like Alphabet (GOOGL), Microsoft (MSFT), and Amazon (AMZN), all of which are buying up semiconductors, real estate, and data center hardware at a blistering pace to satisfy surging demand for artificial intelligence.

The companies have vigorously defended their investment, saying underspending on AI and falling behind competitors is a far greater risk than overspending. Meta’s (META) better-than-expected results on Wednesday eased some of the Street’s fears, but disappointing results from Amazon on Thursday reignited the debate about AI spending.

A Shaky Economy Has Investors on Edge

At the same time, investors are becoming increasingly concerned about the state of the economy. Fed Chair Jerome Powell may have opened the door to a September rate cut at a press conference earlier this week, but a relatively abrupt slowdown in the labor market has some wondering if it’s not already too late.

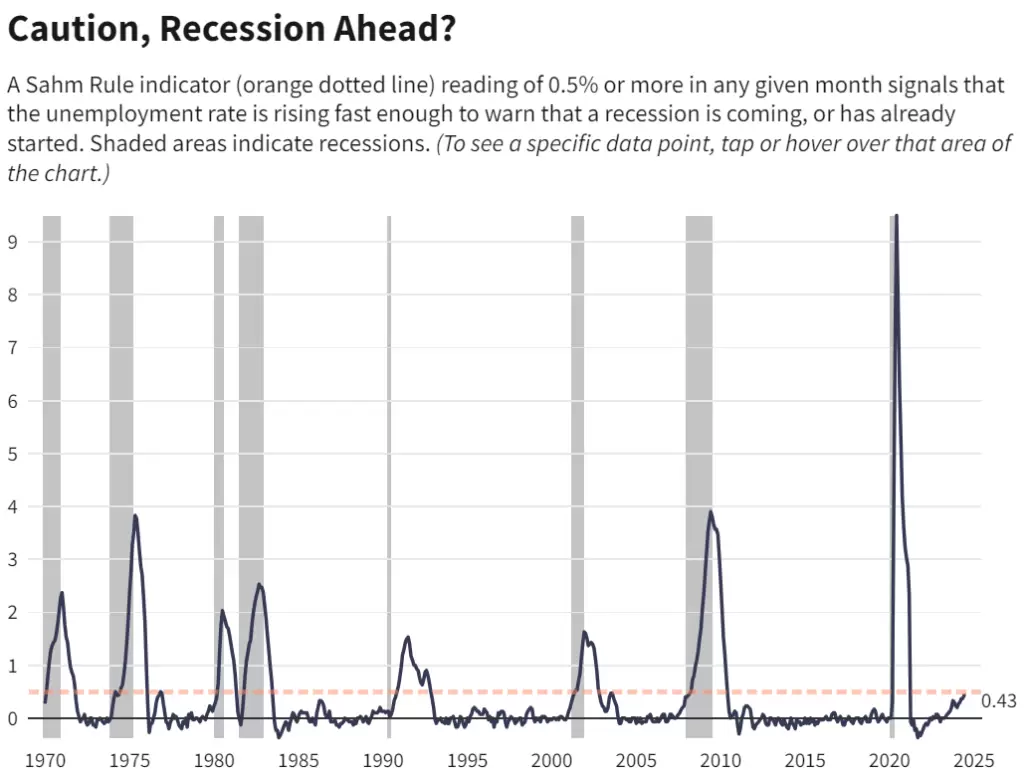

Friday’s jobs report triggered the Sahm rule, a recession indicator that is based on how quickly the unemployment rate increases.

Powell, when asked about the rule earlier this week, noted that plenty of other indicators, like the inverted yield curve, have for some time signaled a recession that hasn’t come.

“What we think we’re seeing is a normalizing labor market,” he said, pointing to strong but slowing wage growth and fewer vacancies as evidence of the job market’s rebalancing.

“We’re watching carefully to see if it turns out to be more,” he added, referring to the labor market’s cooldown. If Friday’s report seems to the Fed to be evidence of a more dramatic deterioration in the labor market, Powell said the central bank is “well-positioned to respond.“

After Friday’s jobs data, financial markets are pricing 125 basis points, or 1.25 percentage points, of rate cuts by the end of 2024, up from 75 basis points the day before, according to the CME Group’s FedWatch tool, which forecasts interest rate movements based on fed funds futures trading data. The likelihood priced in of a half-point cut at the September FOMC meeting is now around 72%, up from 22% on Thursday.